Introduction

The structure of a country’s tax code is a determining factor of its economic performance. A well-structured tax code is easy for taxpayers to comply with and can promote economic development while raising sufficient revenue for a government’s priorities. In contrast, poorly structured tax systems can be costly, distort economic decision-making, and harm domestic economies.

Many countries have recognized this and have reformed their tax codes. Over the past few decades, marginal tax rates on corporate and individual income have declined significantly across the Organisation for Economic Co-operation and Development (OECD). Now, most OECD nations raise a significant amount of revenue from broad-based taxes such as payroll taxes and value-added taxes (VAT).[1]

Not all recent changes in tax policy among OECD countries have improved the structure of tax systems; some have made a negative impact. Though some countries like the United States and France have reduced their corporate income tax rates by several percentage points, others, like Turkey, have increased them. Corporate tax base improvements have occurred in Chile and the United Kingdom, while the corporate tax base has been made less competitive in Belgium.

The COVID-19 pandemic has led many countries to adopt temporary changes to their tax systems. Faced with revenue shortfalls from the downturn, countries will need to consider how to best structure their tax systems to foster both an economic recovery and raise revenue.

The variety of approaches to taxation among OECD countries creates a need to evaluate these systems relative to each other. For that purpose, we have developed the International Tax Competitiveness Index—a relative comparison of OECD countries’ tax systems with respect to competitiveness and neutrality.

The International Tax Competitiveness Index

The International Tax Competitiveness Index (ITCI) seeks to measure the extent to which a country’s tax system adheres to two important aspects of tax policy: competitiveness and neutrality.

A competitive tax code is one that keeps marginal tax rates low. In today’s globalized world, capital is highly mobile. Businesses can choose to invest in any number of countries throughout the world to find the highest rate of return. This means that businesses will look for countries with lower tax rates on investment to maximize their after-tax rate of return. If a country’s tax rate is too high, it will drive investment elsewhere, leading to slower economic growth. In addition, high marginal tax rates can impede domestic investment and lead to tax avoidance.

According to research from the OECD, corporate taxes are most harmful for economic growth, with personal income taxes and consumption taxes being less harmful. Taxes on immovable property have the smallest impact on growth.[2]

Separately, a neutral tax code is simply one that seeks to raise the most revenue with the fewest economic distortions. This means that it doesn’t favor consumption over saving, as happens with investment taxes and wealth taxes. It also means few or no targeted tax breaks for specific activities carried out by businesses or individuals.

As tax laws become more complex, they also become less neutral. If, in theory, the same taxes apply to all businesses and individuals, but the rules are such that large businesses or wealthy individuals can change their behavior to gain a tax advantage, this undermines the neutrality of a tax system.

A tax code that is competitive and neutral promotes sustainable economic growth and investment while raising sufficient revenue for government priorities.

There are many factors unrelated to taxes which affect a country’s economic performance. Nevertheless, taxes play an important role in the health of a country’s economy.

To measure whether a country’s tax system is neutral and competitive, the ITCI looks at more than 40 tax policy variables. These variables measure not only the level of tax rates, but also how taxes are structured. The Index looks at a country’s corporate taxes, individual income taxes, consumption taxes, property taxes, and the treatment of profits earned overseas. The ITCI gives a comprehensive overview of how developed countries’ tax codes compare, explains why certain tax codes stand out as good or bad models for reform, and provides important insight into how to think about tax policy.

Due to some data limitations, recent tax changes in some countries may not be reflected in this year’s version of the International Tax Competitiveness Index.

2022 Rankings

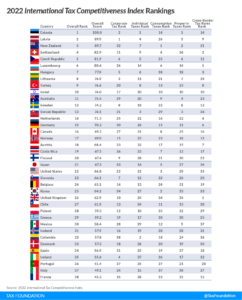

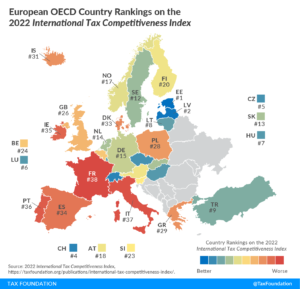

For the ninth year in a row, Estonia has the best tax code in the OECD. Its top score is driven by four positive features of its tax system. First, it has a 20 percent tax rate on corporate income that is only applied to distributed profits. Second, it has a flat 20 percent tax on individual income that does not apply to personal dividend income. Third, its property tax applies only to the value of land, rather than to the value of real property or capital. Finally, it has a territorial tax system that exempts 100 percent of foreign profits earned by domestic corporations from domestic taxation, with few restrictions.

| Country | Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|---|

| 🇪🇪 Estonia | 1 | 100 | 2 | 1 | 14 | 1 | 14 |

| 🇱🇻 Latvia | 2 | 89.9 | 1 | 4 | 26 | 5 | 9 |

| 🇳🇿 New Zealand | 3 | 89.7 | 32 | 7 | 1 | 2 | 21 |

| 🇨🇭 Switzerland | 4 | 82.9 | 11 | 9 | 4 | 36 | 2 |

| 🇨🇿 Czech Republic | 5 | 81.9 | 6 | 5 | 25 | 6 | 11 |

| 🇱🇺 Luxembourg | 6 | 80.6 | 26 | 14 | 6 | 14 | 5 |

| 🇭🇺 Hungary | 7 | 77.9 | 5 | 6 | 38 | 18 | 3 |

| 🇱🇹 Lithuania | 8 | 76.9 | 3 | 11 | 31 | 7 | 24 |

| 🇹🇷 Turkey | 9 | 76.6 | 20 | 8 | 13 | 23 | 8 |

| 🇮🇱 Israel | 10 | 76 | 17 | 30 | 10 | 10 | 10 |

| 🇦🇺 Australia | 11 | 75.5 | 29 | 20 | 9 | 4 | 23 |

| 🇸🇪 Sweden | 12 | 74.2 | 8 | 18 | 22 | 8 | 12 |

| 🇸🇰 Slovak Republic | 13 | 74.1 | 21 | 3 | 29 | 3 | 34 |

| 🇳🇱 Netherlands | 14 | 71.3 | 25 | 22 | 16 | 22 | 4 |

| 🇩🇪 Germany | 15 | 70.2 | 30 | 26 | 15 | 11 | 6 |

| 🇨🇦 Canada | 16 | 69.3 | 27 | 31 | 8 | 25 | 16 |

| 🇳🇴 Norway | 17 | 69 | 15 | 23 | 23 | 16 | 13 |

| 🇦🇹 Austria | 18 | 68.6 | 23 | 32 | 17 | 15 | 7 |

| 🇨🇷 Costa Rica | 19 | 67.5 | 36 | 33 | 7 | 12 | 17 |

| 🇫🇮 Finland | 20 | 67.4 | 9 | 28 | 21 | 20 | 22 |

| 🇯🇵 Japan | 21 | 67.3 | 33 | 16 | 5 | 27 | 26 |

| 🇺🇸 United States | 22 | 66.8 | 22 | 21 | 3 | 29 | 35 |

| 🇸🇮 Slovenia | 23 | 66.1 | 7 | 12 | 32 | 26 | 20 |

| 🇧🇪 Belgium | 24 | 65.1 | 14 | 13 | 24 | 31 | 19 |

| 🇰🇷 Korea | 25 | 64.1 | 34 | 27 | 2 | 33 | 33 |

| 🇬🇧 United Kingdom | 26 | 62.9 | 10 | 24 | 34 | 34 | 1 |

| 🇨🇱 Chile | 27 | 61.9 | 13 | 34 | 11 | 13 | 38 |

| 🇵🇱 Poland | 28 | 59.3 | 12 | 10 | 35 | 32 | 29 |

| 🇬🇷 Greece | 29 | 59.2 | 19 | 17 | 30 | 30 | 25 |

| 🇲🇽 Mexico | 30 | 58.4 | 28 | 29 | 12 | 9 | 37 |

| 🇮🇸 Iceland | 31 | 57.9 | 16 | 19 | 28 | 28 | 31 |

| 🇨🇴 Colombia | 32 | 57.8 | 38 | 2 | 18 | 24 | 36 |

| 🇩🇰 Denmark | 33 | 57.3 | 18 | 36 | 20 | 19 | 30 |

| 🇪🇸 Spain | 34 | 56.9 | 31 | 25 | 19 | 37 | 18 |

| 🇮🇪 Ireland | 35 | 55.6 | 4 | 37 | 36 | 17 | 32 |

| 🇵🇹 Portugal | 36 | 51.4 | 37 | 35 | 27 | 21 | 28 |

| 🇮🇹 Italy | 37 | 49.1 | 24 | 15 | 37 | 38 | 27 |

| 🇫🇷 France | 38 | 45.3 | 35 | 38 | 33 | 35 | 15 |

While Estonia’s tax system is the most competitive in the OECD, the other top countries’ tax systems receive high scores due to excellence in one or more of the major tax categories. Latvia, which recently adopted the Estonian system for corporate taxation, also has a relatively efficient system for taxing labor income. New Zealand has a relatively flat, low-rate individual income tax that also largely exempts capital gains (with a combined top rate of 39 percent), a well-structured property tax, and a broad-based VAT. Switzerland has a relatively low corporate tax rate (19.7 percent), a low, broad-based consumption tax, and an individual income tax that partially exempts capital gains from taxation. Luxembourg has a broad-based consumption tax and a competitive international tax system.

France has the least competitive tax system in the OECD. It has a wealth tax on real estate, a financial transaction tax, and an inheritance tax. The French VAT covers less than 50 percent of final consumption, revealing both policy and enforcement gaps.

Countries that rank poorly on the ITCI often levy relatively high marginal tax rates on corporate income or have multiple layers of tax rules that contribute to complexity. Four of the five countries at the bottom of the rankings all have higher than average corporate tax rates. Ireland ranks poorly on the ITCI despite its low corporate tax rate. This is due to high personal income and dividend taxes and a relatively narrow VAT base. In addition, the five lowest-ranking countries have high consumption tax rates, with rates of 20 percent or higher.

Notable Changes from Last Year[3]

Czech Republic 🇨🇿

The Czech Republic increased the top tax rate on personal income from 15 percent to 27 percent. The Czech Republic’s ranking fell from 4th to 5th.

France 🇫🇷

France has been reducing its corporate income tax rate over several years, a process which concludes in 2022. As part of this scheduled reduction, France dropped its combined corporate rate (including a surtax) from 28.41 percent in 2021 to 25.83 percent in 2022. Its Index rank remained unchanged at 38.

Ireland 🇮🇪

Prior to 2022, Ireland did not have a limit on interest deductions. Now interest is limited to 30 percent of earnings before interest, depreciation, and amortization. There is an exemption for borrowing costs below €3 million. Ireland’s rank fell from 28 to 35.

Italy 🇮🇹

Italy repealed its patent box and replaced it with a 110 percent super deduction for research and development spending. Italy’s rank remained at 37.

New Zealand 🇳🇿

New Zealand increased its top personal income tax rate from 33 percent to 39 percent. New Zealand’s ranking remained unchanged at 3.

Turkey 🇹🇷

Turkey reduced its corporate income tax rate from 25 percent in 2021 to 23 percent in 2022. Turkey’s rank rose from 9th to 4th.

United Kingdom 🇬🇧

The UK introduced a temporary 130 percent super-deduction for plant and equipment. The UK’s ranking increased from 27 to 26.

| Country | 2020 Rank | 2020 Score | 2021 Rank | 2021 Score | 2022 Rank | 2022 Score | Change in Rank from 2021 to 2022 | Change in Score from 2021 to 2022 |

|---|---|---|---|---|---|---|---|---|

| Australia | 10 | 77.1 | 9 | 76.2 | 11 | 75.5 | -2 | -0.6 |

| Austria | 17 | 70.7 | 16 | 70.6 | 18 | 68.6 | -2 | -1.9 |

| Belgium | 20 | 69.6 | 25 | 65.4 | 24 | 65.1 | 1 | -0.3 |

| Canada | 16 | 71.7 | 18 | 69.7 | 16 | 69.3 | 2 | -0.4 |

| Chile | 35 | 58.3 | 26 | 62.5 | 27 | 61.9 | -1 | -0.5 |

| Colombia | 29 | 61.2 | 35 | 56.3 | 32 | 57.8 | 3 | 1.5 |

| Costa Rica | 21 | 69 | 20 | 67.9 | 19 | 67.5 | 1 | -0.4 |

| Czech Republic | 4 | 85.5 | 4 | 84.3 | 5 | 81.9 | -1 | -2.4 |

| Denmark | 32 | 60.1 | 34 | 57 | 33 | 57.3 | 1 | 0.3 |

| Estonia | 1 | 100 | 1 | 100 | 1 | 100 | 0 | 0 |

| Finland | 24 | 68.4 | 21 | 67.8 | 20 | 67.4 | 1 | -0.4 |

| France | 38 | 43.3 | 38 | 45 | 38 | 45.3 | 0 | 0.3 |

| Germany | 14 | 72.4 | 15 | 71.5 | 15 | 70.2 | 0 | -1.3 |

| Greece | 34 | 58.8 | 33 | 58.6 | 29 | 59.2 | 4 | 0.6 |

| Hungary | 7 | 78.6 | 7 | 78.3 | 7 | 77.9 | 0 | -0.3 |

| Iceland | 28 | 61.6 | 31 | 59 | 31 | 57.9 | 0 | -1 |

| Ireland | 30 | 61.1 | 28 | 60.5 | 35 | 55.6 | -7 | -4.8 |

| Israel | 11 | 75.6 | 10 | 75.2 | 10 | 76 | 0 | 0.8 |

| Italy | 37 | 50.6 | 37 | 49 | 37 | 49.1 | 0 | 0.1 |

| Japan | 19 | 70 | 17 | 69.7 | 21 | 67.3 | -4 | -2.4 |

| Korea | 25 | 67.9 | 24 | 67.1 | 25 | 64.1 | -1 | -3 |

| Latvia | 3 | 89.9 | 2 | 90.2 | 2 | 89.9 | 0 | -0.3 |

| Lithuania | 8 | 77.5 | 8 | 77.3 | 8 | 76.9 | 0 | -0.4 |

| Luxembourg | 6 | 81.1 | 6 | 80.9 | 6 | 80.6 | 0 | -0.3 |

| Mexico | 33 | 59.2 | 29 | 59.6 | 30 | 58.4 | -1 | -1.2 |

| Netherlands | 15 | 72 | 14 | 72 | 14 | 71.3 | 0 | -0.7 |

| New Zealand | 2 | 90.8 | 3 | 88.9 | 3 | 89.7 | 0 | 0.8 |

| Norway | 18 | 70.3 | 19 | 69.3 | 17 | 69 | 2 | -0.3 |

| Poland | 31 | 60.6 | 30 | 59.5 | 28 | 59.3 | 2 | -0.2 |

| Portugal | 36 | 54 | 36 | 53.3 | 36 | 51.4 | 0 | -1.8 |

| Slovak Republic | 12 | 74.4 | 11 | 74.8 | 13 | 74.1 | -2 | -0.7 |

| Slovenia | 23 | 68.4 | 23 | 67.3 | 23 | 66.1 | 0 | -1.2 |

| Spain | 26 | 64.4 | 32 | 58.9 | 34 | 56.9 | -2 | -1.9 |

| Sweden | 13 | 73.9 | 12 | 74.2 | 12 | 74.2 | 0 | 0.1 |

| Switzerland | 5 | 83.6 | 5 | 83.7 | 4 | 82.9 | 1 | -0.8 |

| Turkey | 9 | 77.4 | 13 | 74 | 9 | 76.6 | 4 | 2.7 |

| United Kingdom | 27 | 61.7 | 27 | 61.1 | 26 | 62.9 | 1 | 1.8 |

| United States | 22 | 68.5 | 22 | 67.7 | 22 | 66.8 | 0 | -0.9 |

Methodological Changes

Each year we review the data and methodology of the Index for ways that could improve how it measures both competitiveness and neutrality. This year we have incorporated several changes to the way the Index treats corporate taxes, individual taxes, consumption taxes, and cross-border tax rules.

We have applied each change to prior years to allow consistent comparison across years. Data for all years using the current methodology is accessible in the GitHub repository for the Index,[4] and a description of how the Index is calculated is provided in the Appendix of this report. Prior editions of the Index, however, are not comparable to the results in this 2022 edition due to these methodological changes.

General

Costa Rica was added to this year’s Index as it became the 38th member of the Organisation for Economic Co-operation and Development (OECD) in 2021.

The Index previously relied on some measures of tax complexity that were developed by PwC in conjunction with the World Bank’s Doing Business report. In September 2021, that report was discontinued. The Index no longer uses any variables from that report or PwC’s “Paying Taxes” study. Instead, new measures of tax complexity have been included as described below.

Corporate Tax

The prior tax complexity measures have been replaced with three new measures for complexity. The first is a tally of tax rates that apply to corporate income. These rates could arise because corporate income is taxed at different rates due to business size or the size of business profits, or because there is an alternative minimum tax that sits alongside normal corporate tax rules. The second measure is the rate of a corporate surtax if any exists. The third is the amount of revenue collected on corporate or personal income from taxes apart from standard taxes on those lines of income.

Individual Taxes

The prior tax complexity measures for individual taxes have also been replaced with two new measures for complexity. The first is the rate of a corporate surtax if any exists. The second is the amount of revenue collected for social security or through payroll taxes other than standard taxes of that form.

Consumption Taxes

The complexity measure for consumption taxes has been removed as no suitable replacement for the prior measure was found to be compatible.

Cross-Border Tax Rules

In 2017, the United States adopted a unique approach to taxing foreign earnings of U.S. businesses. That approach has been partially incorporated into the design of a global minimum tax proposal. Starting this year, the Index is including another layer to the CFC rules variable which identifies whether a jurisdiction has a form of the minimum tax, which is currently only true of the U.S.

Anti-abuse provisions of this nature are not currently accounted for in the Index. However, if they were appropriately accounted for, countries like Australia, the United Kingdom, and the United States would likely receive worse scores on their cross-border tax rules—potentially also impacting their overall ranking on the Index.

Country Profiles

Australia 🇦🇺

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 11 | 75.5 | 29 | 20 | 9 | 4 | 23 |

Australia ranks 11th overall on the 2022 International Tax Competitiveness Index, two places worse than in 2021. Learn more about the Australian tax system here.

✔️ Some strengths of the Australian tax system:

- Property taxes in Australia are assessed on the value of the land rather than real estate or other improvements to land.

- Australia’s corporate and individual taxes have an integrated treatment of dividends, alleviating the burden of double taxation on distributed earnings.

- Australia ranks well on consumption taxes due to its low goods and services tax (GST) rate but applies it to a relatively narrow base.

❌ Some weaknesses of the Australian tax system:

- Australia’s treaty network consists of just 45 countries, when the average among OECD countries is 74.

- The corporate tax rate in Australia is 30 percent, above the OECD average (23.6 percent).

- Corporations are limited in their ability to write off investments.

Austria 🇦🇹

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 18 | 68.6 | 23 | 32 | 17 | 15 | 7 |

Austria ranks 18th overall on the 2022 International Tax Competitiveness Index, two places worse than in 2021. Learn more about the Austrian tax system here.

✔️ Some strengths of the Austrian tax system:

- Austria’s international tax system is relatively competitive as it is fully territorial without any country limitations, has a broad tax treaty network of 89 countries, and Controlled Foreign Corporation rules that only apply to subsidiaries that do not have substantial economic activity.

- The VAT in Austria applies to a broad base.

- There are no estate, inheritance, or wealth taxes.

❌ Some weaknesses of the Austrian tax system:

- The headline corporate rate of 25 percent is slightly above the OECD average (23.6 percent).

- Austria implemented a digital services tax (DST) in 2020.

- The tax wedge on labor is the 3rd highest among OECD countries.

Belgium 🇧🇪

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 24 | 65.1 | 14 | 13 | 24 | 31 | 19 |

Belgium ranks 24th overall on the 2022 International Tax Competitiveness Index, one spot better than in 2021. Learn more about the Belgium tax system here.

✔️ Some strengths of the Belgium tax system:

- Belgium has a broad tax treaty network, with 95 countries, and a territorial tax system as it fully exempts foreign-sourced dividends and capital gains without any country limitations.

- Capital gains resulting from normal management of private wealth are exempt from tax.

- Belgium provides an allowance for corporate equity (ACE) to address the debt bias that is inherent to the standard corporate income tax.

❌ Some weaknesses of the Belgium tax system:

- The corporate rate of 25 percent is slightly above average among OECD countries (23.6 percent).

- Belgium levies an estate tax and a financial transaction tax and introduced a new annual tax on securities accounts.

- The Belgian tax wedge on labor is the highest among the OECD countries, with the average wage single worker facing a tax burden of 52.6 percent.

Canada 🇨🇦

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 16 | 69.3 | 27 | 31 | 8 | 25 | 16 |

Canada ranks 16th overall on the 2022 International Tax Competitiveness Index, two spots better than in 2021. Learn more about the Canadian tax system here.

✔️ Some strengths of the Canadian tax system:

- Consumption taxes are low, though the consumption tax base is relatively narrow.

- Canada allows businesses to immediately write off investments in machinery.

- Canada does not levy wealth, estate, or inheritance taxes.

❌ Some weaknesses of the Canadian tax system:

- The personal tax on dividends is 39.3 percent, well above the OECD average of 24.2 percent.

- Canada taxes capital gains at a rate of 26.75 percent, while the OECD average is 19 percent.

- The corporate rate of 26.2 percent is above average among OECD countries (23.6 percent).

Chile 🇨🇱

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 27 | 61.9 | 13 | 34 | 11 | 13 | 38 |

Chile ranks 27th overall on the 2022 International Tax Competitiveness Index, one spot worse than in 2021. Learn more about the Chilean tax system here.

✔️ Some strengths of the Chilean tax system:

- As a response to the COVID-19 pandemic, Chile temporarily allows businesses to immediately write off investments in buildings and machinery and to immediately amortize intangibles.

- Chile temporarily reduced its corporate income tax rate to 10 percent for smaller businesses.

- Chile has the second lowest tax wedge on labor among OECD countries, at 7 percent, compared to the OECD average of 34.6 percent.

❌ Some weaknesses of the Chilean tax system:

- Chile has a relatively small tax treaty network with just 33 treaties.

- The tax rate on capital gains is 40 percent, well above the OECD average of 19 percent.

- Chile has a worldwide tax system, while most OECD countries have territorial provisions.

Colombia 🇨🇴

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 32 | 57.8 | 38 | 2 | 18 | 24 | 36 |

Colombia ranks 32nd overall on the 2022 International Tax Competitiveness Index, three places better than in 2021. Learn more about the Colombian tax system here.

✔️ Some strengths of the Colombian tax system:

- A worker earning the nation’s average wage faces the lowest tax burden in the OECD.

- Colombia taxes dividends and capital gains at very low rates.

- While capital gains resulting from inheritance and gifts received are subject to a 10 percent tax, there is no comprehensive estate or inheritance tax.

❌ Some weaknesses of the Colombian tax system:

- The VAT base is very narrow, covering less than 40 percent of Colombian consumption.

- Colombia levies a net wealth tax and a financial transactions tax.

- At 35 percent, Colombia’s corporate income tax rate is significantly above the OECD average (23.6 percent).

Costa Rica 🇨🇷

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 19 | 67.5 | 36 | 33 | 7 | 12 | 17 |

Costa Rica ranks 19th overall on the 2022 International Tax Competitiveness Index, one place better than in 2021. Learn more about the Costa Rican tax system here.

✔️ Some strengths of the Costa Rican tax system:

- Costa Rica has neither a net wealth nor an estate tax.

- The VAT rate is just 13 percent, below the OECD average of 19 percent.

- Capital gains and dividends are both taxed at rates below the OECD average.

❌ Some weaknesses of the Costa Rican tax system:

- Costa Rica has just three tax treaties while the average in the OECD is 74.

- Costa Rica has five separate tax brackets for corporate income.

- At 30 percent, Costa Rica’s corporate income tax rate is significantly above the OECD average (23.6 percent).

Czech Republic 🇨🇿

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 5 | 81.9 | 6 | 5 | 25 | 6 | 11 |

The Czech Republic ranks 5th overall on the 2022 International Tax Competitiveness Index, one place worse than in 2021. Learn more about the Czech tax system here.

✔️ Some strengths of the Czech tax system:

- The corporate rate of 19 percent is below the OECD average (23.6 percent), with above-average cost recovery provisions.

- Taxes on labor are minimally distortive.

- The Czech Republic has a territorial tax system, exempting both foreign dividend and capital gains income from other European countries, combined with a broad tax treaty network.

❌ Some weaknesses of the Czech tax system:

- The VAT threshold is relatively high, contributing to a distortionary VAT design.

- Net operating losses can only be carried forward for five years (they can, however, also be carried back for two years).

- The Czech Republic’s thin capitalization rules are among the stricter ones in the OECD.

Denmark 🇩🇰

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 33 | 57.3 | 18 | 36 | 20 | 19 | 30 |

Denmark ranks 33rd overall on the 2022 International Tax Competitiveness Index, one place better than in 2021. Learn more about the Danish tax system here.

✔️ Some strengths of the Danish tax system:

- Corporate income taxes are relatively less complex than in other countries.

- Denmark has a territorial tax system, exempting both foreign dividend and capital gains income for its treaty partners and other European countries.

- Property taxes are modest, and Denmark allows property taxes to be deducted against corporate income tax.

❌ Some weaknesses of the Danish tax system:

- In addition to a top statutory personal income tax rate of 55.9 percent (including the surtax), the personal income tax rates on dividends and capital gains are both at 42 percent, well above the OECD averages of 24.2 percent and 19 percent, respectively.

- Net operating losses can be carried forward indefinitely but are limited to 60 percent of taxable income if they exceed a certain amount.

- Denmark uses First-In-First-Out for assessing the cost of inventory for tax purposes.

Estonia 🇪🇪

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 1 | 100 | 2 | 1 | 14 | 1 | 14 |

Estonia ranks 1st overall on the 2022 International Tax Competitiveness Index, the same as in 2021, and for the ninth consecutive year. Learn more about the Estonian tax system here.

✔️ Some strengths of the Estonian tax system:

- Estonia’s corporate income tax system only taxes distributed earnings, allowing companies to reinvest their profits tax-free.

- The VAT applies to a broad base and has a low compliance burden.

- Property taxes only apply to the value of land.

❌ Some weaknesses of the Estonian tax system:

- Estonia has tax treaties with just 61 countries, below the OECD average (74 countries).

- Estonia’s territorial tax system is limited to European countries.

- Estonia’s thin capitalization rules are among the more stringent ones in the OECD.

Finland 🇫🇮

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 20 | 67.4 | 9 | 28 | 21 | 20 | 22 |

Finland ranks 20th overall on the 2022 International Tax Competitiveness Index, one place better than in 2021. Learn more about the Finnish tax system here.

✔️ Some strengths of the Finnish tax system:

- Finland has a relatively low corporate tax rate of 20 percent.

- The design of corporate and personal income taxes makes them relatively less complex than in other countries.

- Finland has a territorial tax system and a broad tax treaty network with 76 countries.

❌ Some weaknesses of the Finnish tax system:

- Finland levies both an estate and a financial transactions tax.

- Companies are limited in their ability to carry forward net operating losses and are restricted to using First-In-First-Out as the cost accounting method for inventory.

- Finland’s top statutory rate on personal income is relatively high at 51.3 percent (the OECD average is 42.5 percent).

France 🇫🇷

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 38 | 45.3 | 35 | 38 | 33 | 35 | 15 |

France ranks 38th overall on the 2022 International Tax Competitiveness Index, the same as in 2021. Learn more about the French tax system here.

✔️ Some strengths of the French tax system:

- France has above-average cost recovery provisions for investments in machinery, buildings, and intangibles.

- After several years of reductions, France’s corporate tax rate (25.8 percent) is much closer to the OECD average of 23.6 percent.

- France has a broad tax treaty network, with 122 countries.

❌ Some weaknesses of the French tax system:

- France has multiple distortionary property taxes with separate levies on estates, bank assets, financial transactions, and a wealth tax on real estate.

- The tax burden on labor of 47 percent is among the highest for OECD countries.

- A reduced 10 percent tax rate applies to income derived from IP rights through a so-called patent box.

Germany 🇩🇪

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 15 | 70.2 | 30 | 26 | 15 | 11 | 6 |

Germany ranks 15th overall on the 2022 International Tax Competitiveness Index, the same as in 2021. Learn more about the German tax system here.

✔️ Some strengths of the German tax system:

- The VAT rate of 19 percent is near the OECD average (19 percent).

- Germany has a broad tax treaty network, with 96 countries.

- Inventory can receive Last-In-First-Out treatment, the most neutral treatment of inventory costs.

❌ Some weaknesses of the German tax system:

- Germany has the sixth highest corporate income tax rate among OECD countries, at 29.9 percent.

- The corporate tax burden includes a 5.5 percent surtax.

- Companies are limited in the amount of net operating losses they can use to offset income on future or previous tax returns.

Greece 🇬🇷

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 29 | 59.2 | 19 | 17 | 30 | 30 | 25 |

Greece ranks 29th overall on the 2022 International Tax Competitiveness Index, four places better than in 2021. Learn more about the Greek tax system here.

✔️ Some strengths of the Greek tax system:

- The net personal tax rate of 5 percent on dividends is significantly below the OECD average of 24.2 percent.

- The corporate income tax rate of 22 percent is below the OECD average of 23.6 percent.

- Controlled Foreign Corporation rules in Greece are modest and only apply to passive income.

❌ Some weaknesses of the Greek tax system:

- Companies are severely limited in the amount of net operating losses they can use to offset future profits, and companies cannot use losses to reduce past taxable income.

- Greece has a relatively narrow tax treaty network (57 treaties compared to an OECD average of 74 treaties).

- At 24 percent, Greece has one of the highest VAT rates in the OECD on one of the narrowest bases.

Hungary 🇭🇺

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 7 | 77.9 | 5 | 6 | 38 | 18 | 3 |

Hungary ranks 7th overall on the 2022 International Tax Competitiveness Index, the same as in 2021. Learn more about the Hungarian tax system here.

✔️ Some strengths of the Hungarian tax system:

- Hungary has the lowest corporate tax rate in the OECD, at 9 percent.

- Hungary has a flat personal income tax system.

- Controlled Foreign Corporation rules are better-than-average.

❌ Some weaknesses of the Hungarian tax system:

- Companies are severely limited in the amount of net operating losses they can use to offset future profits, and companies cannot use losses to reduce past taxable income.

- Hungary has the highest VAT rate among OECD countries, at 27 percent.

- Hungary levies taxes on estates, real estate transfers, and bank assets.

Iceland 🇮🇸

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 31 | 57.9 | 16 | 19 | 28 | 28 | 31 |

Iceland ranks 31st overall on the 2022 International Tax Competitiveness Index, the same as in 2021. Learn more about the Icelandic tax system here.

✔️ Some strengths of the Icelandic tax system:

- Iceland’s corporate tax rate of 20 percent is below the OECD average of 23.6 percent, and the tax treatment of investments is one of the best in the OECD.

- Corporate and labor taxes are less complex than they are on average in the OECD.

- Iceland has a territorial tax system that fully exempts foreign dividends and capital gains with no country limitations.

❌ Some weaknesses of the Icelandic tax system:

- Companies are limited in the amount of net operating losses they can use to offset future profits, and companies cannot use losses to reduce past taxable income.

- The VAT of 24 percent applies to a relatively narrow tax base.

- Iceland’s Controlled Foreign Corporation rules apply to both passive and active income.

Ireland 🇮🇪

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 35 | 55.6 | 4 | 37 | 36 | 17 | 32 |

Ireland ranks 35th overall on the 2022 International Tax Competitiveness Index, seven spots worse than in 2021. Learn more about the Irish tax system here.

✔️ Some strengths of the Irish tax system:

- Ireland has a low corporate tax rate of 12.5 percent.

- Net operating losses can be carried back one year and carried forward indefinitely, allowing companies to be taxed on their average profitability.

- The tax treaty network (73 treaties) is just below the average of 74 countries.

❌ Some weaknesses of the Irish tax system:

- Ireland’s personal tax rate on dividend income of 51 percent is the highest among OECD countries.

- The VAT rate of 23 percent is one of the highest in the OECD and applies to a relatively narrow tax base.

- Corporations are limited in their ability to write off investments.

Israel 🇮🇱

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 10 | 76 | 17 | 30 | 10 | 10 | 10 |

Israel ranks 10th overall on the 2022 International Tax Competitiveness Index, the same as in 2021. Learn more about the Israeli tax system here.

✔️ Some strengths of the Israeli tax system:

- Net operating losses can be carried forward indefinitely.

- The VAT rate is relatively low at 17 percent and applies to a relatively broad base.

- Israel does not levy wealth or estate taxes.

❌ Some weaknesses of the Israeli tax system:

- Israel has complex incentives that reduce the corporate tax rate to as low as 7.5 percent on certain technology companies.

- The steep progressivity of Israel’s taxes on labor leads to efficiency costs.

- Israel has a relatively narrow tax treaty network, with 58 countries (the OECD average is 74).

Italy 🇮🇹

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 37 | 49.1 | 24 | 15 | 37 | 38 | 27 |

Italy ranks 37th overall on the 2022 International Tax Competitiveness Index, the same as in 2021. Learn more about the Italian tax system here.

✔️ Some strengths of the Italian tax system:

- Italy has above-average cost recovery provisions for investments in intangibles, as well as an allowance for corporate equity (ACE).

- Last-In-First-Out treatment of the cost of inventory is allowed.

- Italy has a broad tax treaty network, with 100 countries.

❌ Some weaknesses of the Italian tax system:

- Italy has multiple distortionary property taxes with separate levies on real estate transfers, estates, and financial transactions, as well as a wealth tax on selected assets.

- The VAT rate of 22 percent applies to the fourth narrowest consumption tax base in the OECD.

- The corporate tax rate of 27.8 percent is above the OECD average of 23.6 percent.

Japan 🇯🇵

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 21 | 67.3 | 33 | 16 | 5 | 27 | 26 |

Japan ranks 21st overall on the 2022 International Tax Competitiveness Index, four places worse than in 2021. Learn more about the Japanese tax system here.

✔️ Some strengths of the Japanese tax system:

- Japan has a low VAT rate of 10 percent.

- The consumption tax base is relatively broad, covering 65 percent of consumption.

- Japan’s personal income tax rate on dividends is 20.3 percent, below the OECD average of 24.2 percent.

❌ Some weaknesses of the Japanese tax system:

- Japan has poor cost recovery provisions for business investments in machinery and buildings.

- Japan has a hybrid international tax system with a 95 percent exemption for foreign dividends and no exemption for foreign capital gains, while many OECD countries have moved to a fully territorial system.

- Companies are severely limited in the amount of net operating losses they can use to offset future profits.

Korea 🇰🇷

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 25 | 64.1 | 34 | 27 | 2 | 33 | 33 |

Korea ranks 25th overall on the 2022 International Tax Competitiveness Index, one spot worse than in 2021. Learn more about the Korean tax system here.

✔️ Some strengths of the Korean tax system:

- Korea has a low VAT of 10 percent that is applied to a relatively broad base.

- Korea has a broad tax treaty network, with 93 countries.

- Business investments in machinery receive better-than-average treatment for corporate write-offs.

❌ Some weaknesses of the Korean tax system:

- Korea has multiple distortionary property taxes with separate levies on real estate transfers, estates, and financial transactions.

- The personal income tax rate on dividends is 44.0 percent (compared to an OECD average of 24.2 percent).

- Korea is one of the few OECD countries that operates a worldwide corporate tax system (rather than a territorial system).

Latvia 🇱🇻

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 2 | 89.9 | 1 | 4 | 26 | 5 | 9 |

Latvia ranks 2nd overall on the 2022 International Tax Competitiveness Index, the same as in 2021. Learn more about the Latvian tax system here.

✔️ Some strengths of the Latvian tax system:

- Latvia’s corporate income tax system only taxes distributed earnings, allowing companies to reinvest their profits tax-free.

- Corporations can deduct property taxes when calculating taxable income.

- Taxes on labor are relatively flat, allowing the government to raise revenue from taxes on workers with very few distortions.

❌ Some weaknesses of the Latvian tax system:

- Latvia’s network of tax treaties includes 62 countries, a relatively low number.

- Latvia’s thin-capitalization rules are among the stricter ones in the OECD.

- The threshold at which the VAT applies is significantly higher than the average VAT threshold for OECD countries.

Lithuania 🇱🇹

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 8 | 76.9 | 3 | 11 | 31 | 7 | 24 |

Lithuania ranks 8th overall on the 2022 International Tax Competitiveness Index, the same as in 2021. Learn more about the Lithuanian tax system here.

✔️ Some strengths of the Lithuanian tax system:

- Business investments in machinery, buildings, and intangibles receive better-than-average tax treatment.

- Lithuania’s corporate tax rate is 15 percent, well below the OECD average of 23.6 percent.

- Lithuania’s taxes on labor are flatter than average, allowing the government to raise revenue from taxes on workers with very few distortions.

❌ Some weaknesses of the Lithuanian tax system:

- Lithuania has tax treaties with just 54 countries, below the OECD average (74 countries).

- Lithuania has both a patent box and a super deduction for Research and Development expenditures.

- Multinational businesses face strict thin capitalization rules.

Luxembourg 🇱🇺

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 6 | 80.6 | 26 | 14 | 6 | 14 | 5 |

Luxembourg ranks 6th overall on the 2022 International Tax Competitiveness Index, the same as in 2021. Learn more about the Luxembourg tax system here.

✔️ Some strengths of the Luxembourg tax system:

- Business investments in machinery and intangibles receive better-than-average tax treatment.

- Luxembourg applies its relatively low VAT rate of 17 percent to nearly 80 percent of final consumption.

- Capital gains are tax-exempt if a movable asset such as shares was held for at least six months, encouraging long-term savings.

❌ Some weaknesses of the Luxembourg tax system:

- Companies are limited in the time period in which they can use net operating losses to offset future profits and are unable to use losses to offset past taxable income.

- Luxembourg has several distortionary property taxes with separate levies on real estate transfers, estates, and corporate net assets.

- Luxembourg has a solidarity tax which acts as a 7 percent surtax on personal income.

Mexico 🇲🇽

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 30 | 58.4 | 28 | 29 | 12 | 9 | 37 |

Mexico ranks 30th overall on the 2022 International Tax Competitiveness Index, one place worse than in 2021. Learn more about the Mexican tax system here.

✔️ Some strengths of the Mexican tax system:

- The personal income tax rate on dividends is 17.1 percent, below the OECD average of 24.1 percent.

- Corporations can deduct property taxes when calculating taxable income.

- Mexico allows for Last-In-First-Out treatment of the cost of inventory.

❌ Some weaknesses of the Mexican tax system:

- Business losses are severely restricted in the amount of profits that can be offset over time.

- The VAT base is the narrowest in the OECD, with only 37 percent of final consumption being taxed.

- Mexico has a higher-than-average corporate tax rate of 30 percent (the OECD average is 23.6 percent).

Netherlands 🇳🇱

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 14 | 71.3 | 25 | 22 | 16 | 22 | 4 |

The Netherlands ranks 14th overall on the 2022 International Tax Competitiveness Index, the same as in 2021. Learn more about the Dutch tax system here.

✔️ Some strengths of the Dutch tax system:

- The Netherlands allows net operating losses to be carried back one year, and the Last-In-First-Out treatment of the cost of inventory is allowed.

- The Netherlands has a territorial tax system exempting both foreign dividends and capital gains and a broad tax treaty network, with 92 countries.

- Corporations can deduct property taxes when calculating taxable income.

❌ Some weaknesses of the Dutch tax system:

- The Netherlands has a progressive tax system with a combined top rate on personal income of 49.5 percent.

- The VAT of 21 percent applies to approximately half of the potential consumption tax base.

- Companies are limited in the time period in which they can use net operating losses to offset future profits.

New Zealand 🇳🇿

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 3 | 89.7 | 32 | 7 | 1 | 2 | 21 |

New Zealand ranks 3rd overall on the 2022 International Tax Competitiveness Index, the same as in 2021. Learn more about the New Zealand tax system here.

✔️ Some strengths of the New Zealand tax system:

- New Zealand allows corporate losses to be carried forward indefinitely and has introduced a temporary one-year carryback provision, allowing businesses to be taxed on their average profitability.

- The VAT of 15 percent applies to nearly the entire potential consumption tax base.

- New Zealand property taxes apply just to the value of land rather than real estate or other improvements to the land.

❌ Some weaknesses of the New Zealand tax system:

- New Zealand has an above-average corporate tax rate of 28 percent (the OECD average is 23.6 percent) and relatively poor cost recovery provisions for business investments.

- New Zealand has a narrow tax treaty network, with 40 countries.

- The cost of inventory can be accounted for using First-In-First-Out method or the average cost method (Last-In-First-Out is not permitted).

Norway 🇳🇴

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 17 | 69 | 15 | 23 | 23 | 16 | 13 |

Norway ranks 17th overall on the 2022 International Tax Competitiveness Index, two places better than in 2021. Learn more about the Norwegian tax system here.

✔️ Some strengths of the Norwegian tax system:

- Norway allows corporate losses to be carried forward indefinitely.

- Norway’s corporate income tax rate of 22 percent is close to the OECD average (23.6 percent).

- Norway has a territorial tax system, with a network of 87 tax treaties.

❌ Some weaknesses of the Norwegian tax system:

- Corporations are limited in their ability to write off investments.

- Norway is one of the few OECD countries that levies a net wealth tax.

- Controlled Foreign Corporation rules are applied to both passive and active income.

Poland 🇵🇱

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 28 | 59.3 | 12 | 10 | 35 | 32 | 29 |

Poland ranks 28th overall on the 2022 International Tax Competitiveness Index, two places better than in 2021. Learn more about the Polish tax system here.

✔️ Some strengths of the Polish tax system:

- Poland has a below-average corporate tax rate of 19 percent (OECD average is 23.6 percent).

- Poland’s taxes on labor are generally flat, allowing the government to raise revenue from taxes on workers with relative low efficiency costs.

- Poland has a broad tax treaty network including 86 countries.

❌ Some weaknesses of the Polish tax system:

- Poland has multiple distortionary property taxes with separate levies on real estate transfers, estates, bank assets, and financial transactions.

- Companies are severely limited in the amount of net operating losses they can use to offset future profits and are unable to use losses to reduce past taxable income.

- Companies can write off just 33.8 percent of the cost of industrial buildings in real terms (the OECD average is 50.7 percent).

Portugal 🇵🇹

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 36 | 51.4 | 37 | 35 | 27 | 21 | 28 |

Portugal ranks 36th overall on the 2022 International Tax Competitiveness Index, the same as in 2021. Learn more about the Portuguese tax system here.

✔️ Some strengths of the Portuguese tax system:

- Corporations can deduct their property taxes from their taxable income, and there is an allowance for corporate equity (ACE).

- Portugal has a territorial tax system, exempting foreign dividend and capital gains income for most countries.

- Portugal provides above-average capital cost write-offs for investments in machinery.

❌ Some weaknesses of the Portuguese tax system:

- Portugal has a high corporate tax rate of 31.5 percent (the OECD average is 23.6 percent).

- Companies are severely limited in the amount of net operating losses they can use to offset future profits and are unable to use losses to reduce past taxable income.

- The VAT at a rate of 23 percent applies to just half of the potential consumption tax base.

Slovak Republic 🇸🇰

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 13 | 74.1 | 21 | 3 | 29 | 3 | 34 |

The Slovak Republic ranks 13th overall on the 2022 International Tax Competitiveness Index, two spots worse than in 2021. Learn more about the Slovakian tax system here.

✔️ Some strengths of the Slovakian tax system:

- The personal income rate on dividends is very low at 7 percent (compared to an OECD average of 24.1 percent).

- The Slovak Republic has better-than-average tax treatment of business investment in machinery, buildings, and intangibles.

- Corporations can deduct property taxes when calculating taxable income.

❌ Some weaknesses of the Slovakian tax system:

- Companies are severely limited in the amount of net operating losses they can use to offset future profits and are unable to use losses to reduce past taxable income.

- The VAT of 20 percent applies to approximately half of the potential consumption tax base.

- The Slovak Republic has both a patent box and a super deduction for Research and Development expenditures, adding to the complexity of the system.

Slovenia 🇸🇮

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 23 | 66.1 | 7 | 12 | 32 | 26 | 20 |

Slovenia ranks 23rd overall on the 2022 International Tax Competitiveness Index, the same as in 2021. Learn more about the Slovenian tax system here.

✔️ Some strengths of the Slovenian tax system:

- Slovenia has a 19 percent corporate tax rate, below the OECD average (23.6 percent).

- Slovenia’s 22 percent VAT applies to a tax base of roughly the OECD average.

- Capital gains taxes are reduced the longer assets are held (a zero percent rate applies after holding an asset for at least 20 years), encouraging long-term savings.

❌ Some weaknesses of the Slovenian tax system:

- Slovenia’s tax treatment of investments in buildings and intangibles is below the OECD average.

- Slovenia has a relatively narrow tax treaty network, with 59 countries, and only a partial territorial tax system.

- Slovenia has multiple distortionary property taxes with separate levies on real estate transfers, estates, and bank assets.

Spain 🇪🇸

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 34 | 56.9 | 31 | 25 | 19 | 37 | 18 |

Spain ranks 34th overall on the 2022 International Tax Competitiveness Index, two places worse than in 2021. Learn more about the Spanish tax system here.

✔️ Some strengths of the Spanish tax system:

- Spain has a territorial tax system that exempts 95 percent of foreign dividends and capital gains income from taxation.

- The Spanish tax treaty network is made up of 95 countries.

- Property taxes can be deducted against corporate income taxes.

❌ Some weaknesses of the Spanish tax system:

- The VAT of 21 percent applies to less than half of the potential consumption tax base.

- Spain has multiple distortionary property taxes with separate levies on real estate transfers, net wealth, estates, and financial transactions.

- Spain has both a patent box and a credit for Research and Development.

Sweden 🇸🇪

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 12 | 74.2 | 8 | 18 | 22 | 8 | 12 |

Sweden ranks 12th overall on the 2022 International Tax Competitiveness Index, the same as in 2021. Learn more about the Swedish tax system here.

✔️ Some strengths of the Swedish tax system:

- Sweden provides for net operating losses to be carried forward indefinitely, allowing for corporations to be taxed on their average profitability.

- Sweden has a territorial tax system that exempts both foreign dividends and capital gains income from taxation without any country limitations.

- Sweden has a broad tax treaty network, with 85 countries.

❌ Some weaknesses of the Swedish tax system:

- Sweden’s personal dividend tax rate and capital gains tax rate are both 30 percent, above the OECD average (24.2 percent for dividends and 19 percent for capital gains).

- Sweden has a top statutory personal income tax rate of 52.3 percent.

- Sweden has Controlled Foreign Corporation rules that apply to both passive and active income.

Switzerland 🇨🇭

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 4 | 82.9 | 11 | 9 | 4 | 36 | 2 |

Switzerland ranks 4th overall on the 2022 International Tax Competitiveness Index, one place better than in 2021. Learn more about the Swiss tax system here.

✔️ Some strengths of the Swiss tax system:

- Switzerland has above-average cost recovery provisions for investments in buildings and intangibles.

- Switzerland has a broad tax treaty network, with 94 countries.

- The Swiss VAT of 7.7 percent applies to a broad base.

❌ Some weaknesses of the Swiss tax system:

- Switzerland has multiple distortionary property taxes with separate levies on real estate transfers, net wealth, estates, assets, and financial transactions.

- Companies are limited in the time period in which they can use net operating losses to offset future profits and are unable to use losses to reduce past taxable income.

- The VAT exemption threshold is almost twice as high as the OECD average.

Turkey 🇹🇷

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 9 | 76.6 | 20 | 8 | 13 | 23 | 8 |

Turkey ranks 9th overall on the 2022 International Tax Competitiveness Index, four places better than in 2021. Learn more about the Turkish tax system here.

✔️ Some strengths of the Turkish tax system:

- Turkey has a territorial tax system exempting foreign dividends and capital gains income without any country limitations.

- The personal income tax on dividends is 20 percent, below the OECD average (24.1 percent).

- Turkey provides an allowance for equity (ACE), addressing the debt bias inherent to the standard corporate income tax.

❌ Some weaknesses of the Turkish tax system:

- Companies are severely limited in the time period in which they can use net operating losses to offset future profits and are unable to use losses to reduce past taxable income.

- Turkey’s VAT rate of 18 percent applies to less than half of the potential tax base.

- Turkey has multiple distortionary property taxes with separate levies on real estate transfers, estates, and financial transactions.

United Kingdom 🇬🇧

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 26 | 62.9 | 10 | 24 | 34 | 34 | 1 |

The United Kingdom ranks 26th overall on the 2022 International Tax Competitiveness Index, one place better than in 2021. Learn more about the UK tax system here.

✔️ Some strengths of the UK tax system:

- The corporate income tax rate is 19 percent, below the OECD average (23.6 percent).

- The UK has a territorial tax system exempting both foreign dividend and capital gains income without any country limitations.

- The UK tax treaty network with 130 countries is the broadest in the OECD.

❌ Some weaknesses of the UK tax system:

- The top personal income tax rate on dividends is 39.35 percent, well above the OECD average (24.2 percent).

- The real property tax burden is among the highest in the OECD.

- The VAT at a rate of 20 percent applies to less than half of the potential consumption tax base.

United States 🇺🇸

| Overall Rank | Overall Score | Corporate Tax Rank | Individual Taxes Rank | Consumption Taxes Rank | Property Taxes Rank | Cross-Border Tax Rules Rank |

|---|---|---|---|---|---|---|

| 22 | 66.8 | 22 | 21 | 3 | 29 | 35 |

The United States ranks 22nd overall on the 2022 International Tax Competitiveness Index, the same as in 2021. Learn more about the U.S. tax system here.

✔️ Some strengths of the U.S. tax system:

- The U.S. provides full expensing for business investments in machinery.

- The U.S. allows for Last-In-First-Out treatment of the cost of inventory.

- Corporations can deduct property taxes when calculating taxable income.

❌ Some weaknesses of the U.S. tax system:

- U.S. states’ sales taxes apply on average to less than a third of the potential tax base.

- The U.S. has a partial territorial system and does not exempt foreign capital gains income.

- The real property tax burden is among the highest in the OECD.

[1] Daniel Bunn, “Sources of Government Revenue in the OECD,” Tax Foundation, Feb. 10, 2022, https://www.taxfoundation.org/publications/sources-of-government-revenue-in-the-oecd/.

[2] Organisation for Economic Co-operation and Development (OECD), “Tax and Economic Growth,” Economics Department Working Paper No. 620, July 11, 2008.

[3] Last year’s scores published in this report can differ from previously published rankings due to both methodological changes and corrections made to previous years’ data.

[4] Tax Foundation, “International Tax Competitiveness Index,” https://github.com/TaxFoundation/international-tax-competitiveness-index

Source: taxfoundation.org

Cool partnership https://shorturl.fm/FIJkD

https://shorturl.fm/N6nl1

https://shorturl.fm/bODKa

https://shorturl.fm/TbTre

https://shorturl.fm/FIJkD

https://shorturl.fm/YvSxU

https://shorturl.fm/9fnIC

https://shorturl.fm/9fnIC

https://shorturl.fm/TbTre

https://shorturl.fm/m8ueY

https://shorturl.fm/a0B2m

https://shorturl.fm/j3kEj

https://shorturl.fm/N6nl1

https://shorturl.fm/j3kEj

https://shorturl.fm/XIZGD

https://shorturl.fm/Xect5

https://shorturl.fm/VeYJe

https://shorturl.fm/PFOiP

https://shorturl.fm/fSv4z

https://shorturl.fm/ypgnt

https://shorturl.fm/Kp34g

https://shorturl.fm/PFOiP

https://shorturl.fm/0oNbA

https://shorturl.fm/0oNbA

https://shorturl.fm/I3T8M

Unlock exclusive rewards with every referral—enroll now! https://shorturl.fm/YHctZ

Unlock exclusive rewards with every referral—enroll now! https://shorturl.fm/MSTLR

Earn up to 40% commission per sale—join our affiliate program now! https://shorturl.fm/Dl86j

Sign up now and access top-converting affiliate offers! https://shorturl.fm/gYsVN

Start earning on autopilot—become our affiliate partner! https://shorturl.fm/kU6ao

Drive sales, collect commissions—join our affiliate team! https://shorturl.fm/aM7Wn

Join our affiliate program today and earn generous commissions! https://shorturl.fm/39V0h

Refer and earn up to 50% commission—join now! https://shorturl.fm/VDIhr

Refer customers, collect commissions—join our affiliate program! https://shorturl.fm/GKUdH

Drive sales and watch your affiliate earnings soar! https://shorturl.fm/483So

Earn up to 40% commission per sale—join our affiliate program now! https://shorturl.fm/dWtH2

Start earning instantly—become our affiliate and earn on every sale! https://shorturl.fm/FBwiJ

Promote our brand and watch your income grow—join today! https://shorturl.fm/WPaR3

Partner with us for generous payouts—sign up today! https://shorturl.fm/RuzyH

Partner with us and earn recurring commissions—join the affiliate program! https://shorturl.fm/609A3

Tap into unlimited earning potential—become our affiliate partner! https://shorturl.fm/OIVXw

Refer friends, earn cash—sign up now! https://shorturl.fm/IaqbH

Partner with us and enjoy high payouts—apply now! https://shorturl.fm/BNjmE

Refer and earn up to 50% commission—join now! https://shorturl.fm/qVBj0

Promote our brand and watch your income grow—join today! https://shorturl.fm/oixs5

Monetize your audience—become an affiliate partner now! https://shorturl.fm/8eDI1

Start earning instantly—become our affiliate and earn on every sale! https://shorturl.fm/tGMOV

Earn passive income on autopilot—become our affiliate! https://shorturl.fm/4FpgD

Join our affiliate community and earn more—register now! https://shorturl.fm/1e2Kc

Your audience, your profits—become an affiliate today! https://shorturl.fm/0liVT

Promote our products and earn real money—apply today! https://shorturl.fm/OA0vU

Become our affiliate—tap into unlimited earning potential! https://shorturl.fm/IgwZB

Share your link and rake in rewards—join our affiliate team! https://shorturl.fm/enD3U

Earn passive income on autopilot—become our affiliate! https://shorturl.fm/y7lXN

Get paid for every referral—sign up for our affiliate program now! https://shorturl.fm/GYEZS

Start sharing, start earning—become our affiliate today! https://shorturl.fm/ghbuH

Share our link, earn real money—signup for our affiliate program! https://shorturl.fm/zzbHH

Join our affiliate program today and start earning up to 30% commission—sign up now! https://shorturl.fm/UT4DN

Monetize your influence—become an affiliate today! https://shorturl.fm/v7HC3

Your audience, your profits—become an affiliate today! https://shorturl.fm/JizrJ

Join our affiliate community and maximize your profits—sign up now! https://shorturl.fm/f1oCr

Refer friends, collect commissions—sign up now! https://shorturl.fm/IF6Ni

Turn your network into income—apply to our affiliate program! https://shorturl.fm/njnCg

Share your link, earn rewards—sign up for our affiliate program! https://shorturl.fm/h9Hq6

Become our partner and turn referrals into revenue—join now! https://shorturl.fm/2brgT

Share our products and watch your earnings grow—join our affiliate program! https://shorturl.fm/uFs3I

Monetize your audience—become an affiliate partner now! https://shorturl.fm/tale7

Share our link, earn real money—signup for our affiliate program! https://shorturl.fm/1wLge

Share our link, earn real money—signup for our affiliate program! https://shorturl.fm/1wLge

Your audience, your profits—become an affiliate today! https://shorturl.fm/kpB7a

https://shorturl.fm/4iYvA

https://shorturl.fm/mZThu

https://shorturl.fm/5sOLG

https://shorturl.fm/vG1K0

https://shorturl.fm/p7OHS

https://shorturl.fm/oAcDQ

https://shorturl.fm/zi209

https://shorturl.fm/PPXVG

https://shorturl.fm/bMtrK

https://shorturl.fm/uygE0

https://shorturl.fm/9rQjj

https://shorturl.fm/4ndpt

https://shorturl.fm/KyP1o

https://shorturl.fm/71cGX

https://shorturl.fm/BmReT

https://shorturl.fm/lCzmC

https://shorturl.fm/oYsWd

https://shorturl.fm/6hzTi

https://shorturl.fm/DpOgm

https://shorturl.fm/lKYbu

https://shorturl.fm/CiWmN

https://shorturl.fm/vofCf

https://shorturl.fm/YJg0p

https://shorturl.fm/rTHS1

https://shorturl.fm/ADN2M

https://shorturl.fm/sYvLz

https://shorturl.fm/xv6jq

https://shorturl.fm/liM32

https://shorturl.fm/kVwWa

https://shorturl.fm/NMMP4

https://shorturl.fm/E89oC

https://shorturl.fm/fvfEz

https://shorturl.fm/p1mBz

https://shorturl.fm/cCPfG

https://shorturl.fm/fjGOL

https://shorturl.fm/XIUlv

https://shorturl.fm/4Asx4

https://shorturl.fm/7LTy1

https://shorturl.fm/ZjAxC

https://shorturl.fm/GX1yN

https://shorturl.fm/r4zeB

https://shorturl.fm/R6PUC

https://shorturl.fm/uIAle

https://shorturl.fm/mos1j

https://shorturl.fm/6N6eJ

https://shorturl.fm/W7DhQ

https://shorturl.fm/Lg6t9

https://shorturl.fm/oUbfT

https://shorturl.fm/VfUCw

https://shorturl.fm/vtxl6

https://shorturl.fm/Eg5tT

https://shorturl.fm/URhM9

https://shorturl.fm/hNVdL

https://shorturl.fm/R0cEy

https://shorturl.fm/ktf0j

https://shorturl.fm/oc5tG

https://shorturl.fm/NdQI3

https://shorturl.fm/pRSnq

https://shorturl.fm/P04Uq

https://shorturl.fm/Vc1s7

https://shorturl.fm/xtQ4B

https://shorturl.fm/4EEzQ

https://shorturl.fm/j8EXT

https://shorturl.fm/i8T8c

https://shorturl.fm/LOCMM

https://shorturl.fm/AnUKU

https://shorturl.fm/31gjB

https://shorturl.fm/JWKJ2

https://shorturl.fm/seO4y

https://shorturl.fm/mAO9y

https://shorturl.fm/6a9Cn

https://shorturl.fm/IBdHR

https://shorturl.fm/CQJrq

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me? https://accounts.binance.info/da-DK/register-person?ref=V3MG69RO

Your article helped me a lot, is there any more related content? Thanks!

Partner with us and earn recurring commissions—join the affiliate program!

Promote our brand and get paid—enroll in our affiliate program!

Start sharing, start earning—become our affiliate today!

Your article helped me a lot, is there any more related content? Thanks!

https://shorturl.fm/fXjpc

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

https://shorturl.fm/KARXY

https://shorturl.fm/dsQkn

https://shorturl.fm/FUsyS

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

https://shorturl.fm/9I7fD

https://shorturl.fm/xWV2p

https://shorturl.fm/GQalu

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

Your article helped me a lot, is there any more related content? Thanks! https://accounts.binance.bh/en/register?ref=JHQQKNKN

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me. https://www.binance.bh/register?ref=L4EUT9FG